How Much Does Speech Therapy Cost? What Families Actually Pay

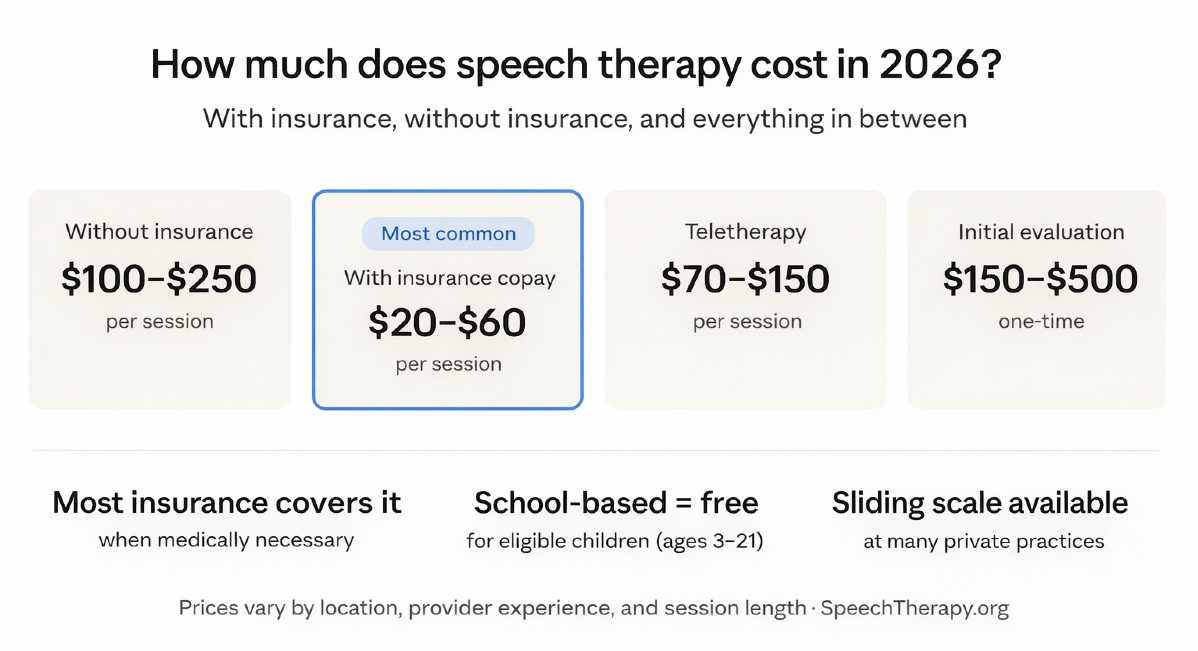

- Private speech therapy typically costs $50 to $175 per session depending on length and location

- Many insurance plans cover speech therapy when it is medically necessary — often reducing cost to $0 to $40 per visit

- Early Intervention for children under three is free or very low cost in every US state

- School-based therapy is free for eligible children ages three through twenty-one

- Medicaid and CHIP cover speech therapy for eligible children at little or no cost

- Speech therapy cost at a glance

- Evaluation costs

- Session costs by length

- Why costs vary so much

- Does insurance cover speech therapy?

- Free and low cost options

- How to verify your benefits and FAQ

Speech Therapy Cost at a Glance

Speech therapy costs vary significantly depending on where services are provided, who is paying, and whether insurance is involved. The table below shows the full range of what families actually pay across different settings — from completely free to several hundred dollars per session.

| Setting | Typical cost to family | Who qualifies |

|---|---|---|

| Early Intervention (birth–3) | Free — federally mandated evaluation. Therapy free or sliding scale. | Children birth to age 2 years 11 months with developmental delay |

| School-based (ages 3–21) | Free for eligible students under an IEP | Children whose speech delay affects educational performance |

| Medicaid / CHIP | Free or very low cost | Children and adults who meet income eligibility requirements |

| Private insurance — in network | $0–$40 copay per session after deductible | Anyone with coverage — requires medical necessity and prior auth |

| Private insurance — out of network | 20–50% of session cost after deductible | Plans with out-of-network benefits — partial reimbursement |

| Private pay — no insurance | $50–$175 per session | Anyone — no eligibility requirements |

| University training clinics | $20–$75 per session | Anyone — sessions led by supervised graduate students |

| Teletherapy | $50–$150 per session — often covered by insurance | Anyone — insurance coverage similar to in-person sessions |

Speech Therapy Evaluation Costs

Before therapy begins most providers require a comprehensive speech and language evaluation. This is a one-time cost that establishes a baseline, identifies the specific areas of need, and produces the documentation required for insurance coverage and school or Early Intervention services.

Speech Therapy Session Costs by Length

Once therapy begins families typically pay per session. Sessions range from 30 to 60 minutes depending on the child’s age, attention span, and goals. For toddlers and young children 30-minute sessions are most common. Longer sessions are more typical for school-age children and adults.

These are private pay rates without insurance. With insurance coverage the out-of-pocket cost per session is typically a copay of $0 to $40 after your deductible is met. For children who qualify for Early Intervention or school-based services the cost is zero.

For a full breakdown of how to access free or low cost speech therapy — including Early Intervention for toddlers — see our complete guide to early intervention speech therapy.

Why Speech Therapy Costs Vary So Much

Two families in the same city can pay dramatically different amounts for speech therapy — one pays nothing, another pays $175 per session. Understanding why costs vary so much helps you find the most affordable path for your situation.

Does Insurance Cover Speech Therapy?

Yes — most insurance plans cover speech therapy when it is considered medically necessary. But what counts as medically necessary varies by insurer, diagnosis, and plan type. Understanding what your plan covers — and what it does not — before you start therapy saves significant money and avoids unexpected bills.

What Insurance Typically Covers

- Initial speech and language evaluation

- Speech sound disorders and articulation

- Language delays with medical diagnosis

- Fluency disorders — stuttering

- Voice disorders

- Swallowing and feeding disorders — dysphagia

- Post-stroke or acquired brain injury therapy

- Autism-related communication therapy

- Neurological conditions — Parkinson’s, TBI

- Teletherapy sessions — same as in-person

- Educational-only services without medical diagnosis

- Mild delays without documented medical necessity

- Social communication therapy without medical justification

- Services from out-of-network providers on some plans

- Accent modification or reduction

- Elective voice training

- Sessions beyond annual visit limits

- Therapy deemed maintenance rather than active progress

- No prior authorization obtained before therapy began — always get this first

- Missing or insufficient documentation — evaluation report, treatment plan, progress notes

- Therapy deemed educational rather than medical — documentation of medical necessity is critical

- Out-of-network provider used without checking plan benefits first

- Annual visit limit reached — track session counts carefully throughout the year

What Insurance Requires for Speech Therapy Coverage

Insurance companies do not automatically cover speech therapy — they require specific documentation and processes to be followed. Missing any of these steps is the most common reason claims are denied.

-

1A physician referral or prescription Most insurance plans require a referral from your primary care physician or pediatrician before speech therapy can begin. Get this before your first session — not after.

-

2A formal speech-language evaluation A comprehensive evaluation report from a licensed SLP is required to establish medical necessity. This report must document the specific diagnosis, standardized test scores, and clinical findings.

-

3Prior authorization before therapy begins Many plans require pre-approval — called prior authorization — before therapy sessions will be covered. Your SLP’s office can typically handle this process but confirm before your first session.

-

4A documented treatment plan with measurable goals Insurance requires a written treatment plan showing specific measurable goals, the frequency of sessions, and the expected duration of therapy. Generic plans are more likely to be questioned.

-

5Periodic progress reports showing active improvement Insurance companies require evidence that therapy is producing measurable progress. Therapy that is deemed maintenance — maintaining skills rather than actively improving them — may be denied coverage.

Understanding Copays, Deductibles, and Coinsurance

Even with insurance coverage most families pay something out of pocket. Understanding how your plan’s cost sharing works helps you budget accurately and avoid surprises.

The most important thing to check is whether your plan uses copays or coinsurance for specialist services — and what your deductible is. A plan with a high deductible effectively means you pay private pay rates until that deductible is met each year. Ask your HR department or insurer for a clear breakdown before therapy begins.

For a full breakdown of how insurance works for developmental speech delays specifically — including the difference between medical and educational coverage — see our guide to early intervention speech therapy.

Free and Low Cost Speech Therapy Options

Before paying private rates out of pocket it is worth knowing that significant free and low cost speech therapy is available to many families — if you know where to look. These are not workarounds or compromises. They are federally funded programs specifically designed to make speech therapy accessible regardless of income.

Federally funded under Part C of IDEA. Available in every US state. Evaluation is always free. Therapy is free or income-based sliding scale. No referral needed — parents can self-refer directly.

- Available birth through age 2 years 11 months

- Free evaluation regardless of income

- Sessions in your home — therapist comes to you

- Parent coaching is central to the program

- Self-refer — no doctor’s referral required

Free for eligible students under an Individualized Education Program — IEP. Focuses on educational impact. Available through your local public school district regardless of whether your child attends public school.

- Free for eligible students ages 3 through 21

- Request an evaluation from your school district in writing

- Services tied to educational goals under an IEP

- May not replace all private therapy needs

- Can be combined with private therapy if needed

Medicaid and the Children’s Health Insurance Program cover speech therapy for eligible children and adults at little or no cost. Coverage is generally strong — often better than private insurance for speech therapy.

- Covers children and adults who meet income eligibility

- Speech therapy typically covered with no visit limits

- CHIP covers children in families above Medicaid limits

- Contact your state Medicaid office to confirm benefits

- EPSDT mandates comprehensive services for children

- 1 Use the CDC’s state-by-state Early Intervention directory to find your local program

- 2 Call and request a free evaluation — no doctor’s referral required in most states

- 3 The program must respond within 45 days — evaluation is completely free

- 4 If eligible therapy begins — free or income-based sliding scale

- 5 Sessions happen in your home — the therapist comes to you

For everything you need to know about Early Intervention — how it works, what sessions look like, and how parents are involved — see our complete guide to early intervention speech therapy.

Other Ways to Reduce Speech Therapy Costs

If free programs do not apply to your situation — or if you need therapy beyond what free programs provide — there are several ways to meaningfully reduce what you pay out of pocket.

Teletherapy — Cost and Coverage

Teletherapy — speech therapy delivered via video call — has become a mainstream option since 2020 and is now covered by most major insurance plans. It is particularly valuable when local wait lists are long, travel is difficult, or you need a specialist not available in your area.

| Option | Typical cost | Notes |

|---|---|---|

| Private insurance — teletherapy | Same copay as in-person | Most major plans cover teletherapy at the same rate as in-person sessions since 2020 |

| Medicaid — teletherapy | Free or very low cost | Most state Medicaid programs cover teletherapy for speech therapy |

| Private pay — teletherapy | $50–$150 per session | Often slightly lower than in-person private rates — no overhead for clinic space |

| Subscription platforms | $150–$300 per month | Some platforms offer subscription models with multiple sessions — verify insurance acceptance |

If You Are Paying Out of Pocket — Tips to Reduce Costs

If private pay is your only option right now here are the most effective ways to reduce what you spend without compromising the quality of care your child or family member receives.

-

1Always check Early Intervention first If your child is under three this is always the first step. It is free, federally mandated, and takes 10 minutes to initiate. There is no reason to pay privately for a child under three before checking EI eligibility.

-

2Ask about sliding scale fees directly Call the clinic and simply ask — do you offer a sliding scale fee or reduced rate for private pay clients? Many do and do not advertise it. The worst they can say is no.

-

3Consider a university training clinic Search for speech-language pathology graduate programs near you and ask if they have a community clinic. Rates are typically a fraction of private practice — and supervision is close and clinical standards are high.

-

4Use your FSA or HSA If you have an employer-sponsored FSA or HSA contribute the maximum allowed and use it to pay for speech therapy. This effectively reduces your cost by 20 to 30 percent depending on your tax bracket.

-

5Invest in parent coaching sessions Instead of weekly therapy sessions consider bi-weekly sessions combined with intensive parent coaching. A parent who carries strategies into every daily routine drives more progress than weekly therapy alone — and costs less.

To find a speech therapist near you — including those who offer sliding scale fees and teletherapy — see our find a speech therapist directory searchable by state.

How to Verify Your Insurance Benefits Before You Start

Verifying your insurance benefits before your first appointment is the single most important step to avoiding surprise bills. Do not assume your plan covers speech therapy — or that the SLP’s office will handle this for you. Here is exactly how to do it.

-

1Call the member services number on your insurance card Ask specifically about speech therapy benefits — not just therapy in general. The coverage for speech therapy can differ significantly from physical or occupational therapy even within the same plan.

-

2Ask about speech therapy for developmental delay specifically Many plans cover speech therapy for medical conditions differently from developmental delays. Ask about both — “Is speech therapy covered for a developmental language delay?” and “Is a medical diagnosis required for coverage?”

-

3Confirm whether prior authorization is required If prior auth is required and you start therapy without it your claims will be denied retroactively. Ask whether authorization is needed before the evaluation as well as before therapy sessions begin.

-

4Ask about your deductible and whether it has been met If your deductible has not been met you will pay the full session cost until it is. Knowing exactly where you stand helps you budget accurately and time the start of therapy strategically if possible.

-

5Ask the SLP’s office to verify benefits as well Most speech therapy practices verify insurance benefits as a routine part of intake. Ask them to do this and share the results with you before your first appointment. Get everything in writing if possible.

-

6Write down the name of the representative and call reference number If a claim is later denied you will need to reference this conversation. Always document who you spoke with, the date, and what you were told. This protects you in the appeals process.

- Is speech therapy covered under my plan — and is a medical diagnosis required?

- Is speech therapy for developmental delay covered differently from other speech therapy?

- Do I need prior authorization before the evaluation — and before therapy sessions?

- How many speech therapy sessions are covered per year?

- What is my deductible and how much of it has been met so far this year?

- What is my copay or coinsurance for specialist services?

- Is teletherapy covered at the same rate as in-person sessions?

- Does the provider I am considering participate in my network?

Frequently Asked Questions

Related Guides

Ready to find a speech therapist?

Search our directory of ASHA-certified speech-language pathologists by state — including providers who accept insurance, offer sliding scale fees, and provide teletherapy.

Always verify your specific benefits directly with your insurance company before beginning therapy.

© 2026 Burke Networks · Editorial Policy